.svg)

Blogs

AI at the Core, Orchestration at the Edge: Strategic Signals from NiCE’s FY2025 Results

February 23, 2026

7 min read

.svg)

.svg)

Blogs

Shivanu Shukla

I joined NiCE’s FY2025 earnings call expecting a routine performance update. What emerged instead was a structural signal about where the customer experience (CX) market is heading.

The FY25 financials were solid (full press release here):

Healthy execution, certainly. But strategically, the message was more profound.

The CX market is transitioning from cloud migration as the growth story to AI monetisation as the growth engine.

For two decades, contact centre success was measured in seats and migrations. The narrative was simple: move from on-prem to cloud, expand licenses, scale volume.

That model is now evolving.

The more telling metric is AI revenue and attach rate: the proportion of enterprise contracts that embed AI as a core component of the platform. NiCE disclosed that AI was included in every new seven-figure deal in FY2025. That is not incremental improvement; it is structural change.

It implies three shifts we are seeing in enterprise behaviour:

We see corroborating signals across the market. Five9 has reported roughly 50% year-over-year growth in enterprise AI revenue (in Q4’25), with $100M in annualised revenue. Genesys continues to highlight accelerating AI ARR alongside cloud momentum. The direction of travel is consistent.

AI is no longer experimental. It is becoming the commercial core of the platform.

A central question hanging over the industry has been whether generative AI will compress agent demand.

Scott Russell, CEO at NiCE, addressed this directly. NiCE is not seeing a dip in agent seats.

This is a critical data point. While AI is driving higher containment and productivity, large enterprises are not yet structurally reducing frontline capacity. Instead, they appear to be reallocating efficiency gains toward more complex and value-intensive interactions.

In complex enterprises, automation augments before it replaces.

Seat contraction may eventually occur in certain segments, but the near-term evidence suggests resilience — not erosion — of human-assisted engagement.

For investors and operators alike, this reframes the thesis. AI is not collapsing the category; it is expanding its economic model.

The most strategically important portion of the call was the emphasis on Cognigy.

Scott referenced Cognigy repeatedly, not as a bolt-on enhancement, but as central to NiCE’s AI strategy.

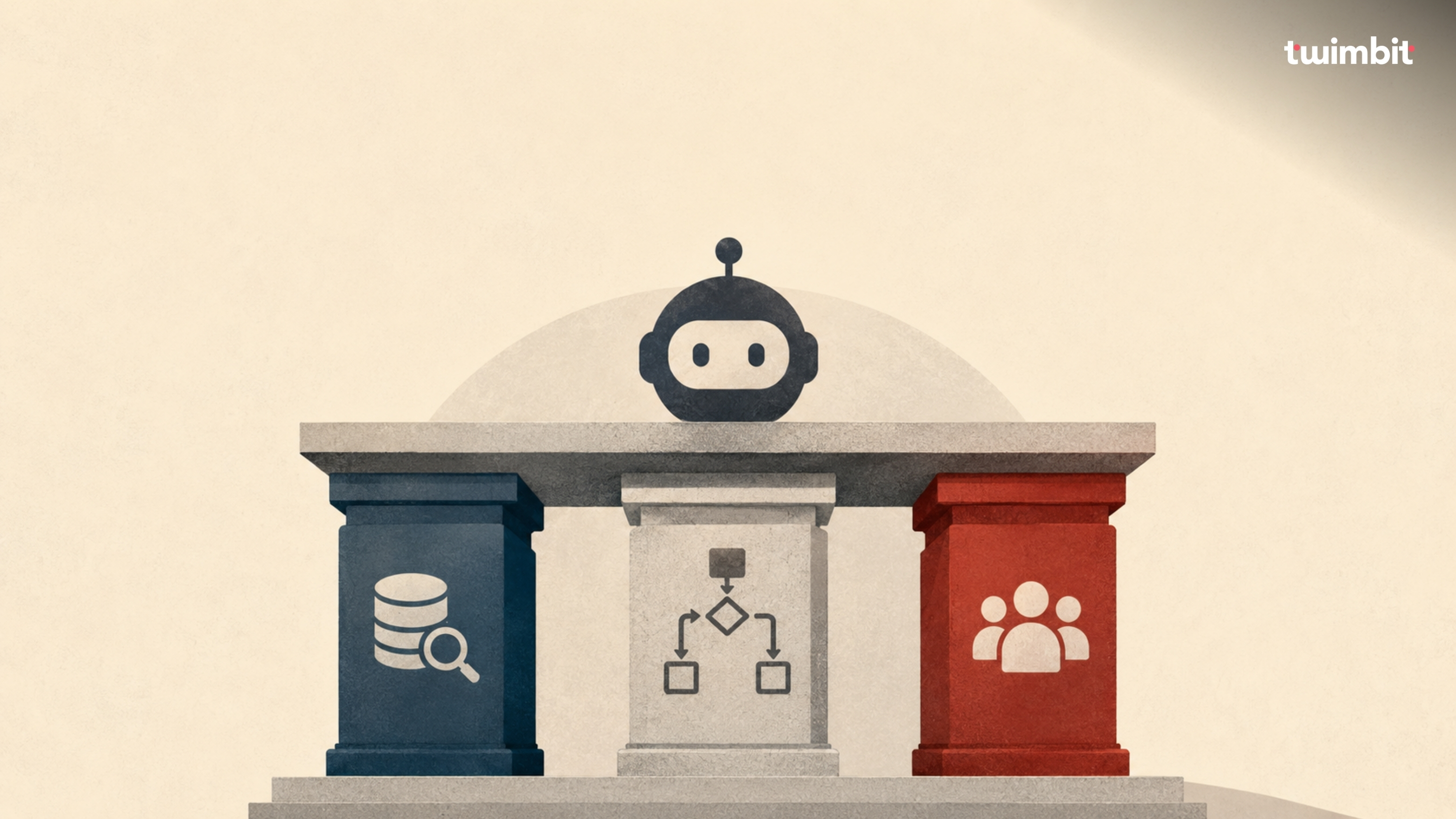

Most enterprises have deployed bots. Very few have achieved enterprise-grade orchestration.

The future of CX will not be determined by who has the most sophisticated generative model. It will be determined by who can orchestrate seamlessly across:

Orchestration is what transforms discrete AI tools into a coherent operating model.

Cognigy strengthens NiCE’s conversational and agentic capabilities. More importantly, it deepens the orchestration layer that sits above channels and below enterprise systems.

This is the battleground. Not chatbot sophistication. Not standalone copilots.

But enterprise-scale orchestration under governance.

Another important takeaway: the migration story is not over.

Despite macro volatility, enterprises continue modernising legacy contact centre infrastructure. On-prem to cloud migration remains active, and in many cases, AI is accelerating the urgency.

This creates a dual growth engine:

Strategically, this matters because AI scales more efficiently in cloud-native environments. Vendors that capture migration flows and then attach AI modules will disproportionately benefit.

Viewed through an international lens, particularly EMEA and Asia Pacific, the orchestration thesis becomes even stronger.

These markets present structural complexity:

In such environments, fragmented AI deployment is untenable. Orchestration is not a premium feature; it is operational infrastructure. Enterprises in these regions require unified platforms that integrate AI, governance, compliance, and performance management across partners and jurisdictions.

Complexity accelerates consolidation toward AI-native orchestration platforms.

Taken together, NiCE’s FY2025 results reinforce three structural shifts in CX:

1. AI attach rate is becoming the primary indicator of platform relevance.

Revenue growth signals scale. AI penetration signals strategic position.

2. Automation is augmenting human capacity before replacing it.

Seat contraction not yet seen at an enterprise scale.

3. Orchestration will determine category leadership.

The winners will be platforms that integrate AI across the full experience lifecycle. Scott Russell’s emphasis on Cognigy suggests NiCE understands this pivot clearly.

The next phase of the CX market will not reward incremental feature releases. It will reward platforms that combine AI penetration with orchestration depth, and convert both into measurable economic value.

AI without orchestration is noise and does not create the right experience. Orchestration without AI is shallow automation.

The competitive advantage lies in combining both and monetising them at scale.

NiCE’s FY2025 performance suggests that the transition is already underway.

Connect to unlock exclusive insights, smart AI tools, and real connections that spark action.

Schedule a chat to unlock the full experience

.svg)

.png)

.svg)