.svg)

Blogs

Jio: A telco or a platform?

June 26, 2026

7 min read

.svg)

.svg)

Blogs

Sanskar Rathee

A telco, or a tech platform? A walk through the numbers, the valuation, and the risks.

Reliance has filed the DRHP for Jio Platforms’ IPO, a fresh issue of up to 27 crore shares, with no offer for sale. It is one of the most anticipated listings India has seen in years. I went through the entire document, along with the accompanying Analysys Mason industry report. Here is what actually matters.

For most of its life, Jio was a spending machine, pouring capital into towers, fibre and spectrum at unprecedented scale, swallowing losses to win a market. The question was always: when does the spending stop and the harvest begin?

The last three years answer it. The build is largely done, and the business has crossed over. Profit now widens each year, because every new customer rides infrastructure that’s already paid for, with operating leverage kicking in. The debt that once defined the company has been worked down, not through fundraising but by out-earning its own appetite for capital. What was consumed by construction now spills out as free cash.

And the customer is changing too: not just joining, but using more, spending more, and staying. The growth is shifting from adding bodies to deepening relationships. Jio is no longer asking you to bet on a network it might build. It has built the network and is now learning how much it can sell through it.

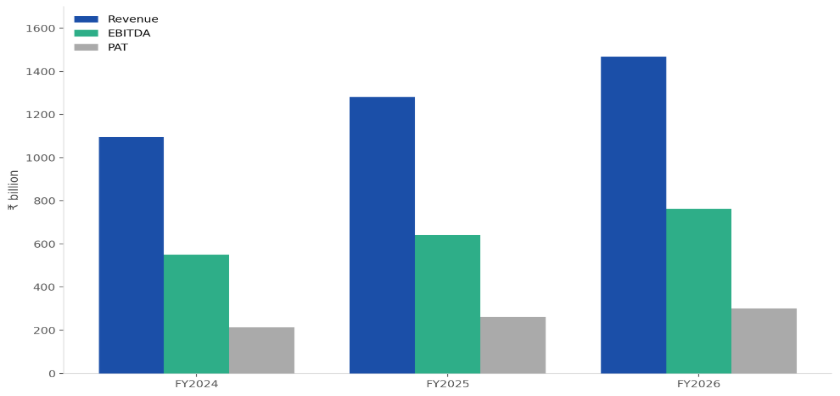

Key financials (FY2024–FY2026)

The deleveraging and the free-cash inflection are the real story: net leverage fell from 0.88x to 0.36x in two years, while EBITDA-less-capex rose roughly 29x. Crucially, this growth is no longer just connectivity. Jio is layering a digital ecosystem of entertainment, cloud, AI, enterprise SaaS, IoT and advertising on top of a network it has already paid to build. That ecosystem, not the GB of data sold, is what will matter over the coming years.

The DRHP shows the price as a placeholder, so we work backwards from the reported issue size.

Building it from the ground up

Step 1: Offer price

Issue size ₹37,700 cr ÷ 27 cr fresh shares = ~₹1,396 per share

Step 2: Post-issue share count

893.9 cr existing + 27 cr fresh = ~920.9 cr shares

Step 3: Implied market cap

₹1,396 × 920.9 cr shares = ~₹12.86 lakh cr (~US$143 bn)

Step 4: The multiples that fall out of it

P/E = ₹1,396 ÷ ₹33.63 (FY26 EPS) = ~41.5x

Price / NAV = ₹1,396 ÷ ₹373.66 = ~3.7x

So at this size, Jio is asking the market to pay roughly 41.5 years of current earnings and nearly four times book value on listing day.

Is 41.5x rich, or fair?

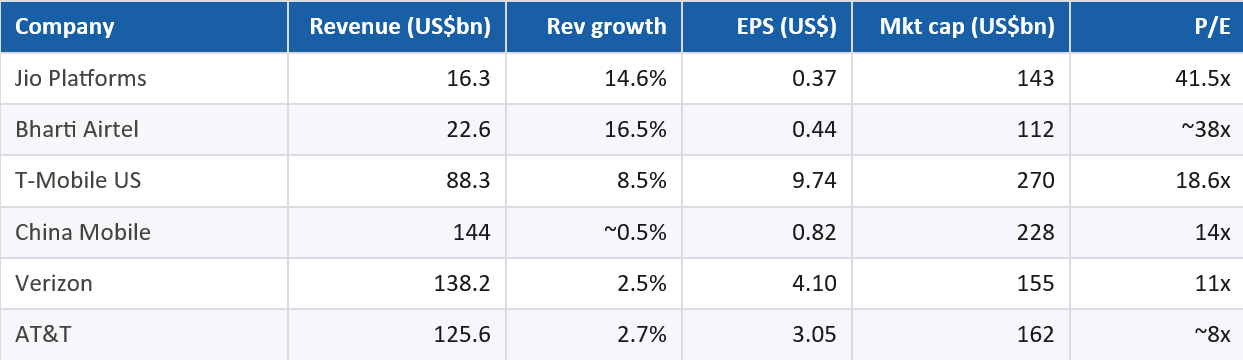

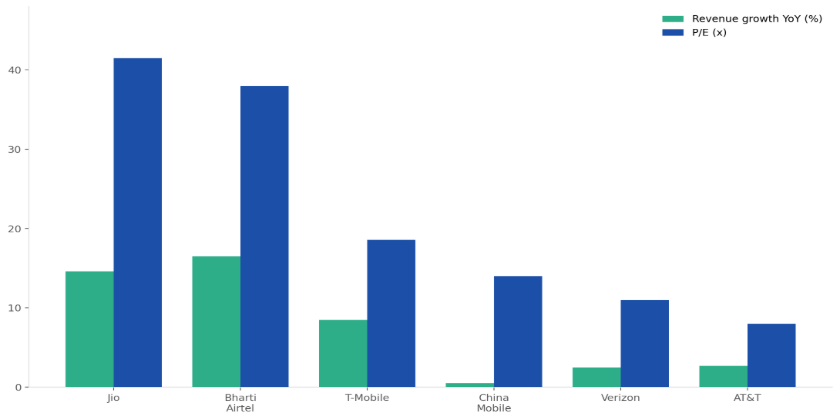

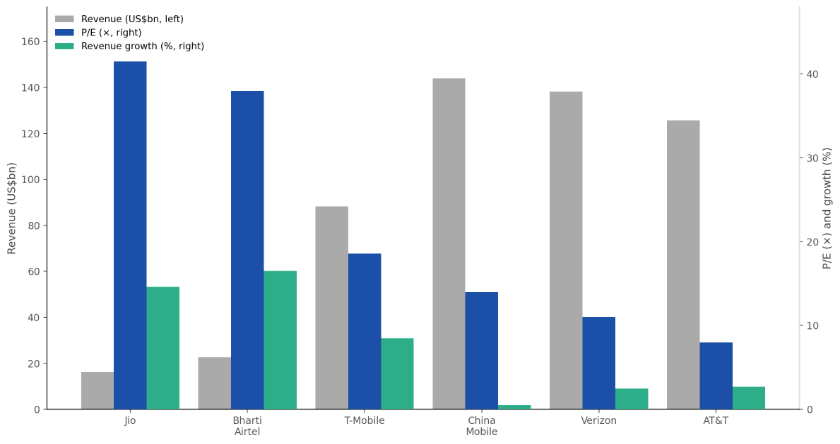

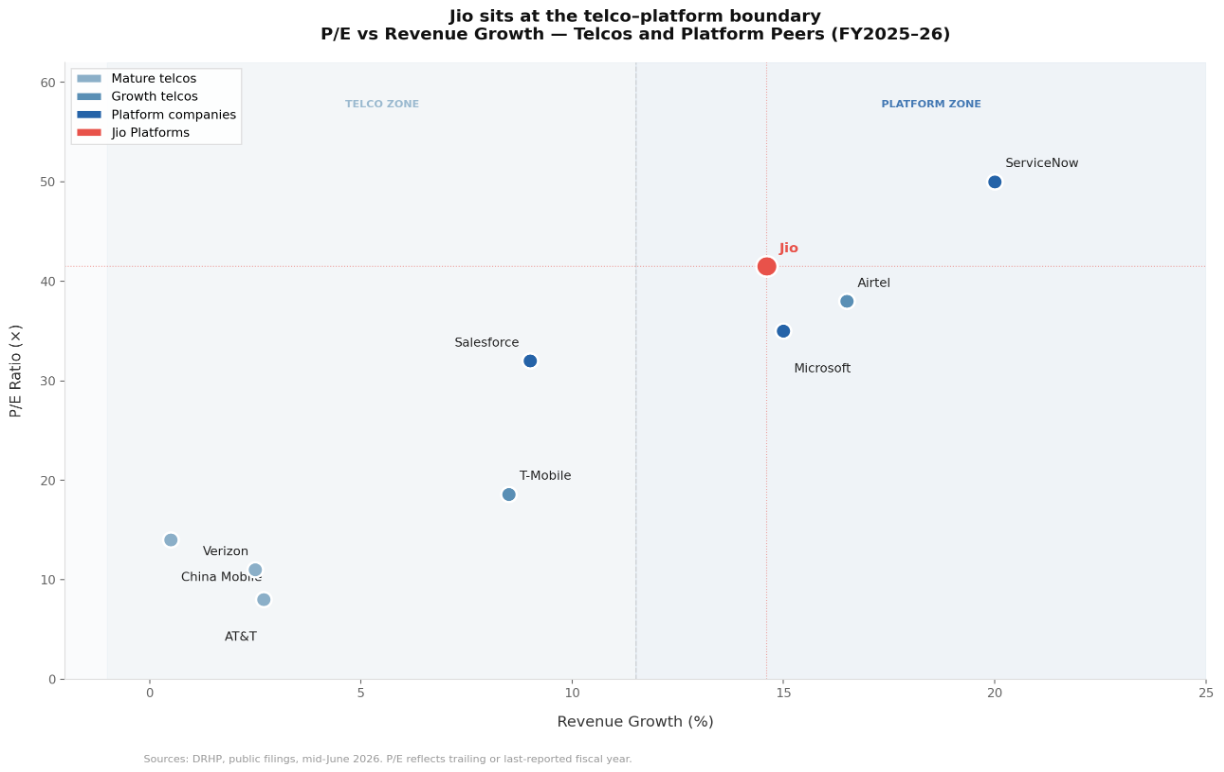

A multiple means nothing in isolation. The only way to judge it is to put Jio next to the companies investors would otherwise own, the world’s large listed telcos, and ask what each one charges for its growth.

The pattern is hard to miss. The mature US and Chinese incumbents are large but barely growing, and the market pays them single-to-low-double-digit multiples for it. Jio is the smallest by revenue, yet it is growing fastest alongside Airtel, and is being valued like the platform it intends to become, not the telco its financials currently describe.

But how does it compare to the companies it is trying to become?

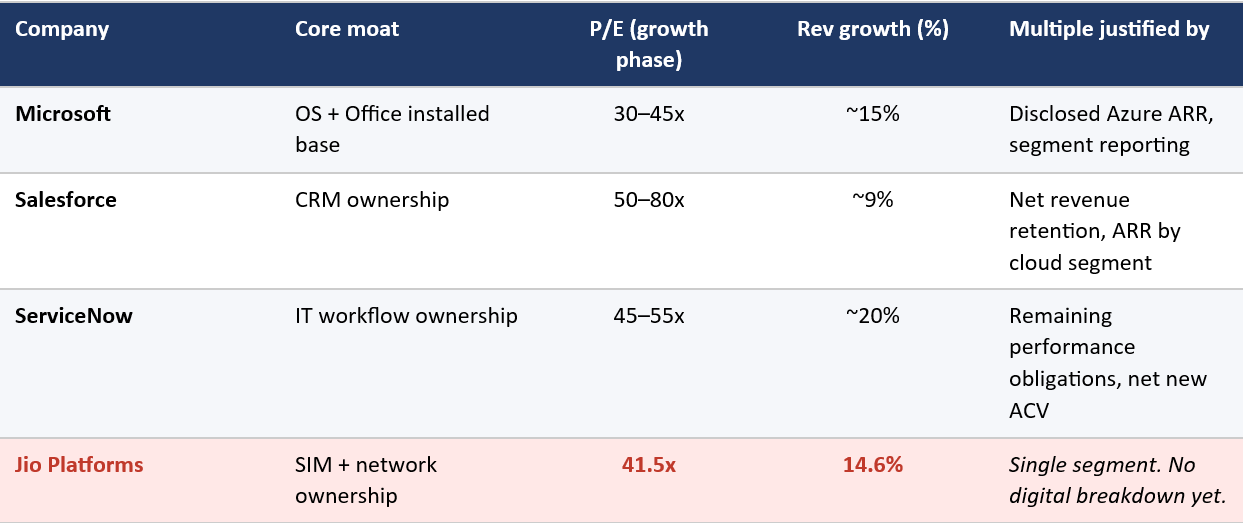

The telco table above tells you what Jio is leaving behind. The more interesting question is what multiple the companies Jio aspires to become actually trade at. Microsoft, Salesforce, and ServiceNow are the three closest structural analogues, each having built an installed customer base at significant upfront cost, then layered high-margin software products on top of that relationship with near-zero incremental acquisition cost. That is precisely the playbook Jio is running.

The chart makes the tension visible. Mature telcos such as AT&T, Verizon and China Mobile cluster in the bottom-left: low growth, low multiples. Platform companies cluster top-right: higher growth rewarded with higher multiples, but crucially, each of them had the segment-level financials to prove it. Jio sits precisely at the boundary, growing like a platform, priced like a platform, but reporting like a telco.

What Microsoft, Salesforce, and ServiceNow share is instructive. Microsoft went from 15x to 45x not because Windows accelerated, but because Azure became a separately reported segment with a disclosed growth rate. Salesforce earned 50–80x by publishing ARR by cloud, specifically Sales Cloud, Service Cloud and Marketing Cloud, so investors could see exactly which products were compounding. ServiceNow trades at 45–55x partly because it discloses remaining performance obligations every quarter, giving the market a forward view of locked-in revenue. In each case, the multiple is not faith, it is forensics. The market is paying for something it can measure.

Jio at 41.5x sits at the floor of the platform range, not the ceiling. That is either a generous starting point, cheap relative to what it could become, or a condition the market will eventually demand be earned. The platform peers suggest the multiple is defensible. The missing disclosure suggests it has not yet been earned. Jio is the first company in this peer group asking for a platform multiple before it has filed a single quarter of digital-services revenue as a separate line item. Microsoft, Salesforce, and ServiceNow all showed the numbers first. The day Jio does the same, the re-rating conversation becomes a great deal more interesting.

My take: Jio isn’t being priced as a telco, and it shouldn’t be. A telco sells data and competes on ARPU. Jio owns 524 million customers, carries roughly 60% of India’s wireless data, and has already absorbed the customer acquisition cost. Every new service it stacks on, from JioAI and JioCloud to JioPC, JioAds and enterprise SaaS for India’s 79 million MSMEs, has near-zero incremental acquisition cost.

It also has a Made-in-India end-to-end 5G stack (one of only five countries globally), addressing a ~US$70 bn global 5G and ~US$145 bn FWA deep-tech export market. That is a technology export play, not a telco play.

The macro tailwind is real

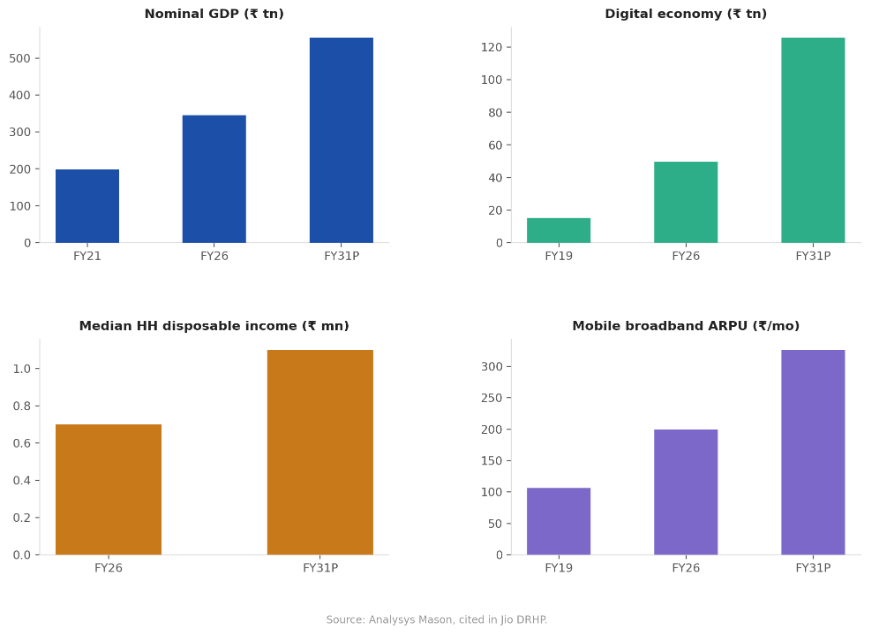

Strip away the CAGRs and one thing is happening: India is crossing the income threshold where digital stops being a luxury and becomes the default.

The disposable income line matters most. Analysys Mason’s math says a household needs roughly ₹8.3 lakh a year before fixed broadband becomes a realistic buy. As median income climbs toward ₹11 lakh, tens of millions of homes cross that line, and they don’t arrive as marginal users. They can suddenly afford the whole bundle: broadband, an OTT stack, cloud, a smart-home device.

The stability metrics are what let that growth compound instead of stuttering. Low inflation keeps rising incomes real. A shrinking deficit and contained current account keep rates lower for longer, which is directly helpful to a company just past a decade of heavy network debt. And five years of US$70 bn-plus FDI is what makes a US$143 bn listing thinkable at all.

The digital economy bar is the destination: it roughly triples by FY2031 and grows from a seventh of the economy to over a fifth. That’s not Jio’s revenue. It’s the size of the pond it fishes in. Jio isn’t betting on a market it must create. The macro is building the demand on its own. Jio’s job is narrower: to be standing at the toll booth when the traffic arrives.

Not the surface-level ones from the risk-factor list. These are the structural ones a careful read surfaces.

1. You don’t fully control the brand or the plumbing.

Jio does not control use of the “Jio” trademark across the Reliance Group, meaning negative publicity from any Group entity flows straight to Jio. It also runs on non-exclusive related-party agreements with RIL and Reliance Retail for key parts of the business. And against the Promoter alone, the DRHP discloses litigation of ₹4,03,106 mn plus US$4.13 bn. As a minority shareholder, you’re buying an entity whose brand, key contracts and reputation sit partly outside its own control.

2. Low leverage hides a dividend constraint.

That clean 0.36x is reassuring, but debt covenants on the ₹7,15,292 mn of borrowings require lender consent for both mergers and dividend declarations. Your ability to receive capital returns is not fully in the company’s hands.

3. The asset-light network is also a dependence.

Jio leans on a limited group of passive infrastructure providers for a substantial share of its towers and fibre. The network you think you’re buying isn’t fully owned. Concentration risk sits underneath the “largest network in India” headline.

And the analytical gap tying it together: today, virtually all revenue is still connectivity, reported as a single segment with no digital-services breakdown. The 41.5x multiple prices in an ecosystem that hasn’t yet appeared in the financials. If monetisation stalls, remember China Mobile, a dominant telco that de-rated to 14x once growth faded.

So what are you buying at 41.5x?

Not a telco. The financials say telco: single segment, connectivity revenue, ARPU and subs. The price says something else. The market is paying a platform multiple for a company that has finished building India’s largest network and is now turning it into a distribution layer for everything else: AI, cloud, commerce, advertising, enterprise software, and a 5G stack it can export.

The bull case: Jio owns 524 million customers it’s already paid to acquire, sits on ~60% of India’s data, and rides a macro backdrop manufacturing demand on its own. If even a few digital verticals scale, today’s multiple looks cheap in hindsight.

The bear case: none of that ecosystem revenue is in the numbers yet. You’re underwriting a transition, not a track record, and the telcos that never made the leap, like China Mobile, trade at a third of Jio’s multiple.

Both are true at once. That’s what makes this the most interesting listing India has seen in years. My read: bullish on the platform Jio is becoming. The day it breaks out digital-services revenue as its own segment, we’ll know whether 41.5x was foresight or faith. Until then, it’s a bet on execution, and Jio’s entire history is a bet on execution that paid off.

Note: The ~₹37,700 cr issue size and ~₹1,396 implied price are estimates used to derive the valuation; the DRHP itself shows the price as a placeholder. Peer multiples are as of mid-June 2026 and will move. This is analysis, not investment advice.

.svg)

.jpg)

.svg)