.svg)

Blogs

Reimagining a new payment wave

February 13, 2025

7 min read

.svg)

.svg)

.jpg)

Blogs

.jpg)

Rashika Sethi

Cross-border transactions, SME payments, and remittances are among the most broken parts of the financial system today. The reasons are clear:

These challenges point to a critical need for faster, more secure, and cost-efficient alternatives—and blockchain has emerged as a strong contender.

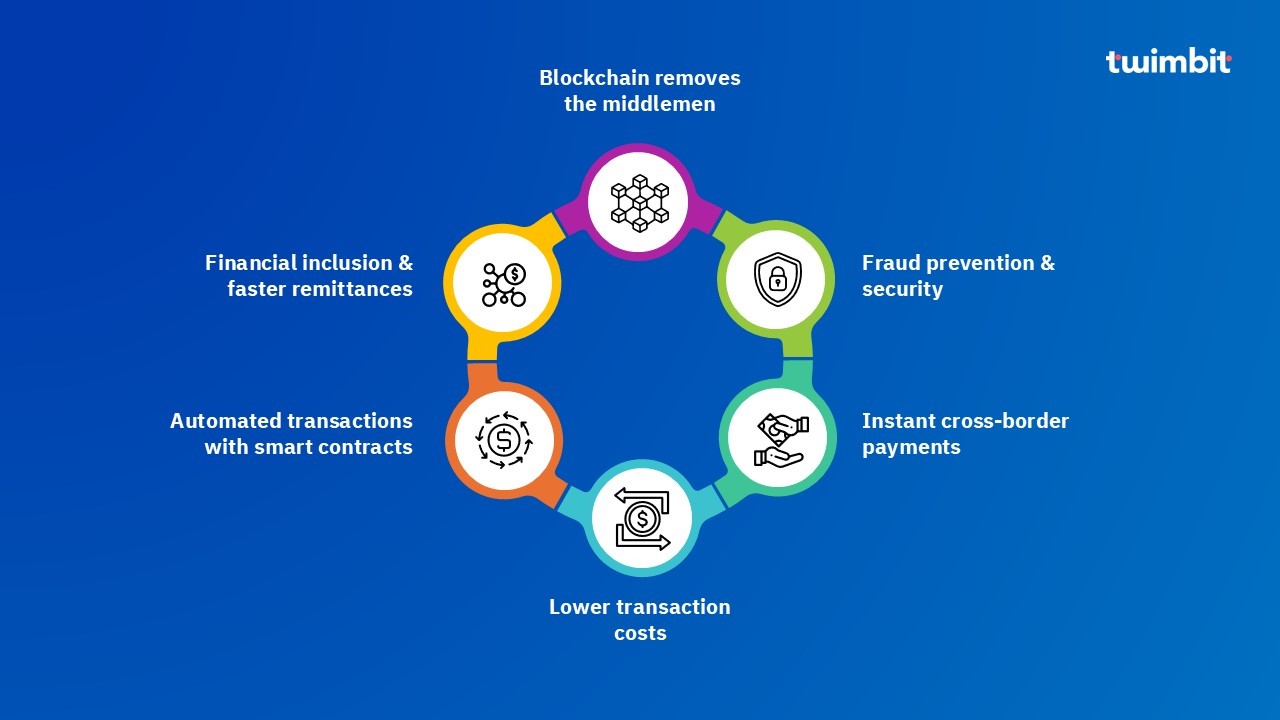

Blockchain technology introduces a trustless, decentralized, and transparent system that solves the inefficiencies of traditional payment networks. Here’s how:

1. Instant cross-border payments

Ripple is a blockchain-based platform designed to make cross-border payments faster, cheaper, and more efficient. It uses its cryptocurrency, XRP, as a bridge currency to facilitate transactions between different currencies. Major banks and payment providers like Santander and American Express are exploring Ripple’s technology for cross-border payments.

2. Lower transaction costs

Note: Stablecoins are type of cryptocurrency pegged to the US Dollar, aiming to maintain a 1:1 value ratio with the currency.

3. Fraud prevention & security

4. SME access to capital & credit

In Singapore, the convergence of technology and finance is unlocking unprecedented opportunities for small and medium enterprises (SMEs). Traditionally, SMEs have struggled to access working capital due to cumbersome processes, lack of trust, and excessive documentation in trade finance. Blockchain technology is now transforming this reality.

Through initiatives like TradeTrust and the Networked Trade Platform (NTP), Singapore has created a seamless, transparent ecosystem for trade finance. These platforms leverage blockchain to digitize critical documents—such as invoices and letters of credit—ensuring traceability and eliminating inefficiencies. Smart contracts further streamline the process by automating payment releases when specific conditions are met.

Consider DBS Bank’s blockchain-enabled solutions, where SMEs can now secure financing in half the time compared to traditional methods. This isn't just about speed; it's about empowering smaller businesses to compete on a global scale, armed with trust and efficiency embedded in every transaction.

Singapore’s example underscores a universal truth: innovation, when harnessed thoughtfully, has the power to level the playing field. Blockchain is more than a technology; it is a catalyst for growth, fostering resilience and inclusivity for SMEs navigating an increasingly interconnected world.

5. Financial inclusion & faster remittances

Despite its promise, blockchain payments haven’t gone fully mainstream yet. Why?

But solutions are emerging—Layer 2 scaling (Polygon, Lightning Network), regulatory frameworks (MiCA in Europe), and CBDCs—paving the way for wider adoption.

Layer 2 scaling refers to technologies built on top of existing blockchain networks to improve their performance, particularly in terms of speed and transaction cost. Layer 2 scaling helps blockchains handle a much higher number of transactions without compromising security or decentralization.

CBDCs are digital versions of a country’s currency, issued and regulated by its central bank. Unlike cryptocurrencies like Bitcoin, CBDCs are centralized and maintain the stability of the local economy.

The transition to blockchain-powered payments is inevitable. Over the next five years, we will see:

The question is no longer if blockchain will redefine payments—it’s when.

.svg)

.jpg)

.svg)