Millennial banking: The next revenue model

This new generation will not tolerate waiting in lines, repeating their problems, or being treated like a number. Companies that do not adapt, risk obsolescence as Millennials become an economic powerhouse. – Joe Gagnon and Jason Dorsey

Who are they?

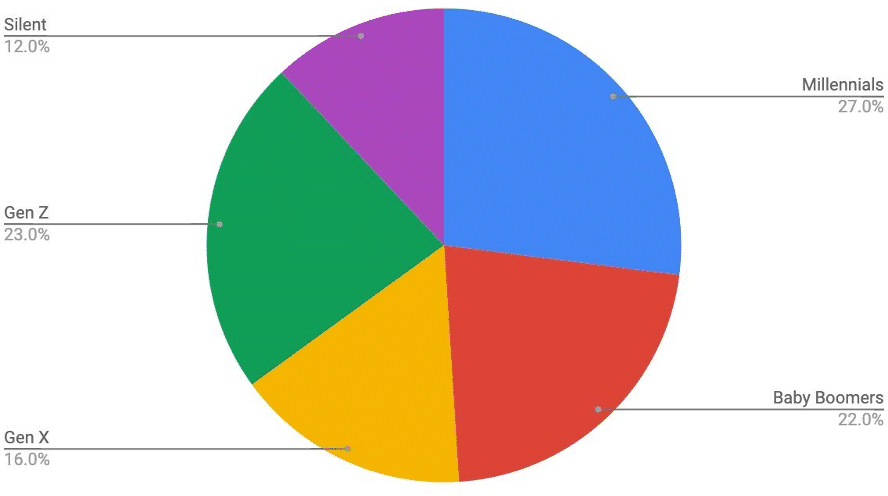

Millennials, also known as Gen Y, are those who fall in the demographic of 18 to 40. This generation not only makes up for 32% of the global population1 but is also expected to account for 65% of the 2global workforce by 20253. Being the largest cohort, millennials will dictate the demand for financial products and services in the ongoing decade which means that they are next in line to inherit the global wealth.

What do they want?

After having understood who they are, it is important to understand their unique needs. Their needs are what makes them so different when compared to other generations. The following are millennials top demands:

- Convenience– Millennials want banks that to be loaded with new-age technologies such as voice assistants, AI functions that understand the user and provide them with a good experience.

- Personalization- Millennials have grown developing attributes of being unique and thus, banks today should focus on personalization with 62% of customers aspiring it, and 83% of them willing to switch institutions if not kept satisfied.

- Investments – Providing access to investment platforms only is not sufficient. Following the above point, millennials want personalized opportunities such as small bite-sized investment plans that can help banks capture the interest of the millennials.

- Reward – The decision of millennials on selecting a bank is based on additional benefits and not just simply stereotypical basic services. User experience is built around the benefits and incentives offered in different ways. for example- Movie tickets, food vouchers, and cashbacks.

- Monetary analytics – Millennials want greater insights about their money along with dashboards which gives a holistic view of their savings, expenditures while providing tips on managing their finances.

Where are banks going wrong?

Banks have been making fortunes for decades, but the digital generation is not happy with what they have to offer. If they want to continue printing money, they will have to provide millennials with the products and services they want. The following are reasons why current banking models are failing:

- Standalone services – Banks fail in embedding themselves in a millennial’s journey by not providing end to end digital services and real-time alerts.

- Traditional Structure – Banks are crafted for the demands of the previous generations. Traditional structures limit these millennials to go beyond standard products and services.

- Failure to Converge – Banks must allow linking of all accounts while keeping an eye on the expense, to be able to break down expenditures into various categories. Millennials want to be able to do everything from the bank’s app itself.

- Lack of innovation – A major technological disruption, a radical change followed by continuous incremental innovations is the need of the hour to meet the new wave of personalized customer experience.

- Lack of financial analytics – To ensure satisfaction, banks need to collaborate with third-party organizations to analyze and purchase surveyed data. Subsequently, they should leverage their power to meet customer financial needs.

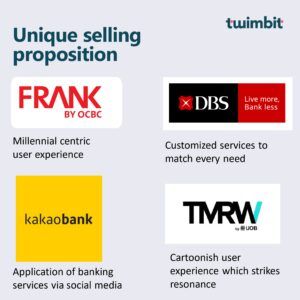

Who’s doing it right?

One bank that in particular has been exceptional in appealing to millennials is OCBC, Singapore. Keeping aside their amazing value proposition in terms of services and products provided, their four unique strategies that have made them successful are as follows:

- Identity – They created an entirely different sub-brand called Frank crafted to meet millennial demand. The stylish name itself has an appeal to it, that the long and boring OCBC acronym does not.

- Location – Their branches are located in millennial centric areas of Singapore, such as university campuses and shopping malls. This not only ensures marketing but also makes them the bank millennials come across every day.

- Outlet – Frank branches are designed as cool cafe’s rather than as boring banks. There are over fifty personalized card designs places all over the wall that individuals while sitting on their fancy tall chairs can feel and play with.

- Website – For starters, their website does not even have an about page. From easy money transfers to opening an account in just a few clicks, Frank by OCBC’s website is one to view.

What have we learnt?

Our key takeaways about millennial banking are as follows:

- Different needs – Firstly, banks need to understand that millennials are not the same as Boomers or Gen X. They are different, they are unique, and thus, their demands can only be met by radical changes.

- Provide utmost ease – Secondly, every service provided to millennials has to be bedded with convenience and the most easily accessible features.

- Constant innovation – Thirdly, millennial’s expectations rise at a greater rate than previous generations. A bank needs to constantly improve and deliver new products and services if they want a slice of the millennial cake.

- Understand behavioral pattern – Lastly, banks have to keep a sharp eye on the change in behavior of millennials as they will not think twice before changing their mind. They need to be understood and then provided with the right services.

References

- https://www.goldmansachs.com/insights/archive/millennials/

- https://www2.deloitte.com/us/en/pages/about-deloitte/articles/millennial-survey-freelance-flexibility.html

- https://www.pwc.com/co/es/publicaciones/assets/millennials-at-work.pdf

- https://www.pewresearch.org/fact-tank/2019/09/09/us-generations-technology-use/

- https://www.canstar.com.au/online-banking/westpac-launches-voice-activated-banking-siri-westpac/

- https://www2.deloitte.com/global/en/pages/aboutdeloitte/articles/millennialsurvey.html

- https://www.tnsglobal.com/sites/default/files/Millennials-on-Phone-A4.pdf