Research highlights:

- Public Cloud spending accounts for approximately 10% of the total IT spend – at least 2.8x more, compared to its Southeast Asian counterparts

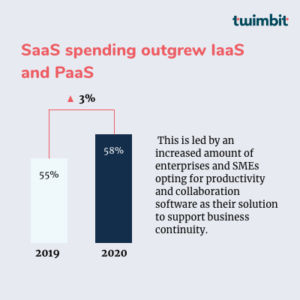

- Software-as-a-Service (SaaS) triumphed in 2020, increasing its share of the market from 55% to 58%. More companies opted for productivity and collaboration software as their solution for business continuity planning

- Notable cloud contracts were witnessed in both leading domestic banks and offshore banks in Singapore as they advanced in their digital transformations, though some remain in favour of hybrid infrastructure environment

- Small Medium Enterprises (SMEs) are leaning towards Chinese cloud providers such as Huawei Cloud and Alibaba Cloud due to price competitiveness – this segment covers 4-5% of the market

Market drivers

Public cloud market benefited from the positive adoption sentiment from both the public and the private sectors and the availability of localized region.

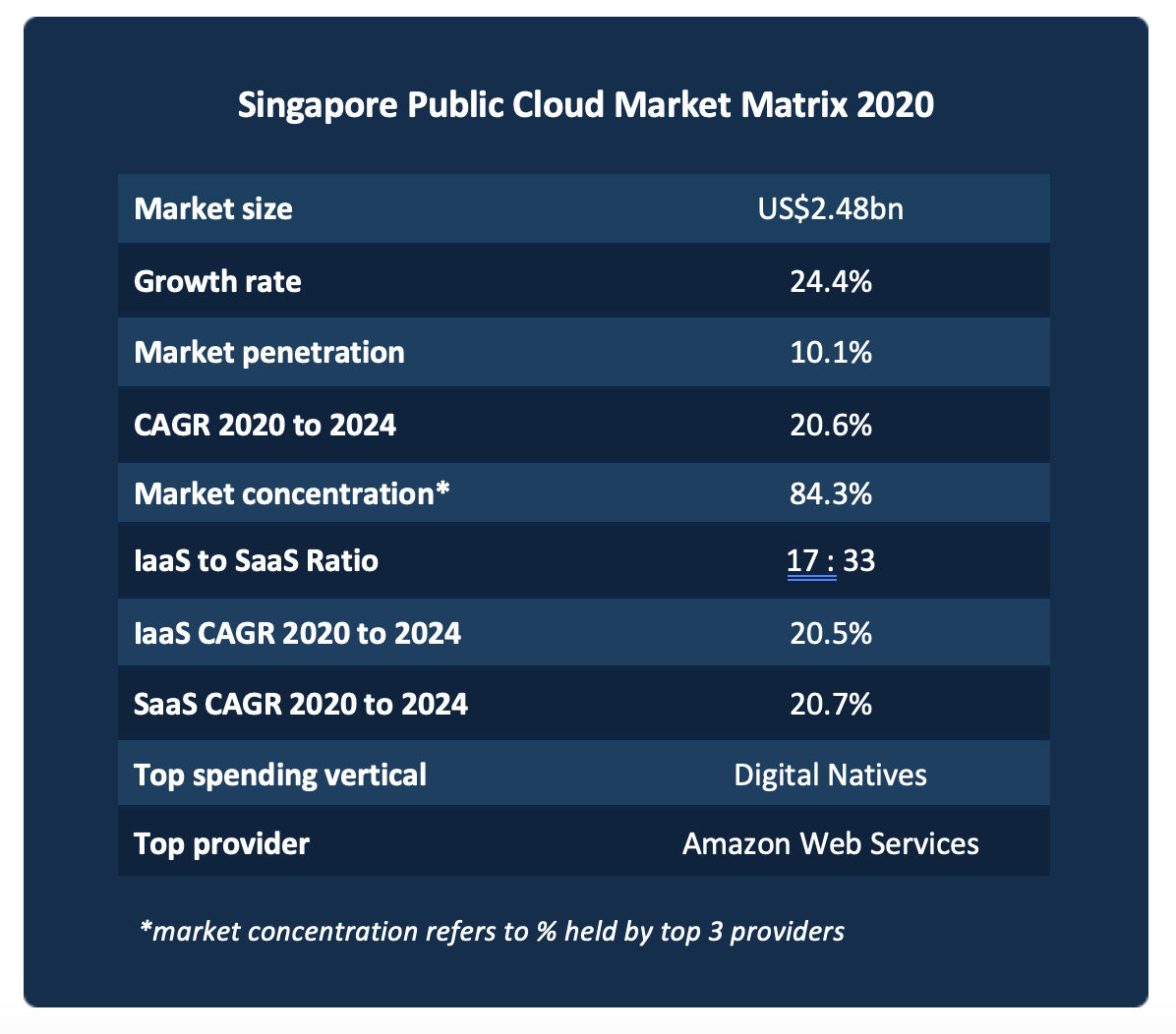

- Digital Natives – Singapore continues to be a favourable destination for emerging and established digital native companies due to reasons such as taxation, funding and ease of business. Undoubtedly, these made Singapore’s public cloud market as one to be watched closely in Asia. These companies account for more than a third of the total market and will continue to drive the market to newer heights.

- Public Sector Support – Government support for the cloud market in the form of policies and adoption are the top reasons why Singapore has set itself apart from most Southeast Asian countries in the area of cloud spending vs. total IT spend. The early adoption by Government agencies, for instance, Land Transport Authority and Immigration and Checkpoint Authority adoption gave confidence to private sectors and combatted certain security concerns. Additionally, clear guidelines and cloud-friendly policies have motivated more providers and partners to expand in the country.

- Migration of Banks – The country holds 3 of the largest banks in Southeast Asia, with a combined market capitalization of US$145 billion. Besides, Singapore houses various leading international banks. The adoption of these banks’ advocates growth for the market. For instance, it was announced this year that DBS Bank is collaborating with AWS to train more than 3,000 of its staff members in AI/ML. It is likely that each of these leading banks is spending between US$19 million to US$25 million on public cloud services.

Market restraints

Unfortunately, due to notable incidents of cyberattacks and security breach in Singapore, the rate of migration has slowed down for enterprises with exposure to classified data and information such as Parkway Hospitals. Many are concerned because of the country’s personal data protection act, which slaps hefty financials penalties in the 6-figure range. However, often, public cloud security is underestimated. Despite a data centre sharing model, leading global providers have made it a point to invest billions to secure the data of its customers with innovative automation. These providers often set a much higher bar than most enterprises when it comes to this. That said, the vulnerability to attacks sometimes lies in the migration to cloud process but it is not at the processing and storage end.

Market size and growth trends

The market growth may vary between 19%-22% y-o-y in the near term

The pandemic has positively impacted the public cloud market in Singapore. More than ever, pressures loom over leadership teams to instil business continuity planning in order to prevent the occurrence of similar predicaments. With that, the conversions of laggards, such as manufacturers, will increase steadily as they seek automation and 24×7 managed services.

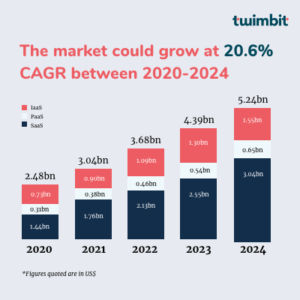

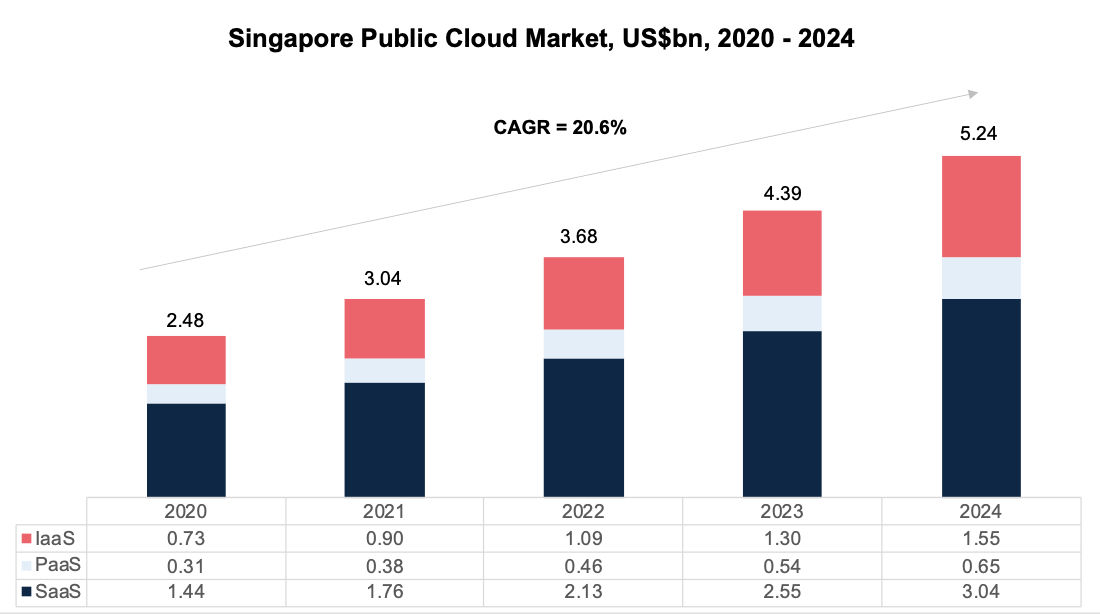

Additionally, Singapore, an island-state with 88.4% internet penetration, will witness an increase in the usage of the cloud by current adopters. Banks will continue to scale their mobile operations while digital native companies will seek to increase the efficacy of their real-time services. Hence, the consumer demand for digital interaction is the main driver for the forecasted 20.6% CAGR between 2020 to 2024.

Trends by key segments

- Public Sector

Singapore’s government is going to continue its five-year cloud migration plan (2020 is the 2nd year), which will allow the market to witness contracts above US$600mn – US$700mn every year for system migration. Also, the government will be increasing grants and widening support coverage for digital transformation amongst SMEs as part of its ‘SMEs Go Digital’ programme during the pandemic.

The public sector could continue to be the top 5 biggest segment in public cloud spend: accounting to about 12-16% each year unless policies and sentiments changes.

- Enterprises & Established Digital Natives

Rightfully so, enterprises and leading digital native companies are the biggest spenders on public cloud, amounting to approximately 72% of the cumulative public cloud market in 2020. This segment may double down on its usage with the objectives of scaling, productivity and innovation as the top motivators.

We may witness a trend of new converters in enterprises and a growing interest in hybrid cloud solution to service data-sensitive industries.

3 things to anticipate in Singapore’s rapidly growing public cloud market

- The aggressive pricing strategy and promotions of newer market entrants to win a larger share of the pie

- Adoption of IaaS could be more widespread as SMEs start its move their applications to the cloud while enterprises witness new converters and increased usage.

- The increased presence of regional cloud consulting and technology partners in Singapore as providers open doors for them

To compare Malaysia public cloud market performance, please click here.